FY25 update

Plenti Group Limited (ASX:PLT) (Plenti) provides this trading update for the quarter ended 31 March 2025 (4Q25).

Highlights

- Cash NPAT of $13.8 million, up 126% on PCP

- Statutory profit of $24.7 million, with underlying statutory profit of $6.4 million

- Loan originations of $1.4 billion, up 18% on PCP

- Closing loan portfolio of $2.5 billion, up 19% on PCP

- Revenue of $259 million, up 23% on PCP

- Robust credit performance, with a 1.10% net loss rate

Plenti delivered on all three elements of its market guidance for FY25 across growth, profitability and efficiency.

Operational highlights

- Materially reduced cost-to-income ratio to 23.9% from 26.5% in PCP, evidencing operating leverage inherent in Plenti's technology-led business model

- Delivered further advancements to Plenti's proprietary technology platform, including significant enhancements to automated credit approvals and integrations with key partners

- Increased repeat and cross-sell originations from existing customers

- Completed three ABS transactions for a record annual issuance of over $1.3 billion

Strategic highlights

- NAB powered by Plenti (NPBP) car loan launched in 2Q25 and subsequently made available to NAB customers via their website, banking app and internet banking from 4Q25

- Launched successful loan subvention program with Tesla, implemented within a three-week period by leveraging the strong integration capabilities of our proprietary technology platform

- Secured up to $60 million in discounted renewable energy funding from the Clean Energy Finance Corporation (CEFC) under its $1 billion Household Energy Upgrades Fund

- Completed successful CEO transition, with Adam Bennett joining as CEO and co-founder Daniel Foggo transitioning to a non-executive director role

- Corporate strategy refreshed, with renewed focus on disciplined, profitable growth in Plenti's three core lending verticals – Automotive, Renewables and Personal Lending

Adam Bennett, Plenti's new CEO, said:

“FY25 was yet another exciting year in Plenti's evolution as we continued to scale into a significant non-bank lender. We successfully changed CEOs whilst our talented team continued to focus on providing great service to our customers, growing the loan book, and driving strong credit and operational outcomes with discipline and enthusiasm.

After my first ten months in role, I'm extremely proud of the team and our accelerating loan book momentum, and it's very pleasing to see our Cash NPAT and statutory NPAT growing significantly as we continue to leverage our scale, proprietary technology, and prime credit posture.

I am extremely excited by the great potential and ambition of this business and remain determined to deliver maximum value through our Automotive, Renewables and Personal Lending businesses as we drive Plenti forward into the coming year.”

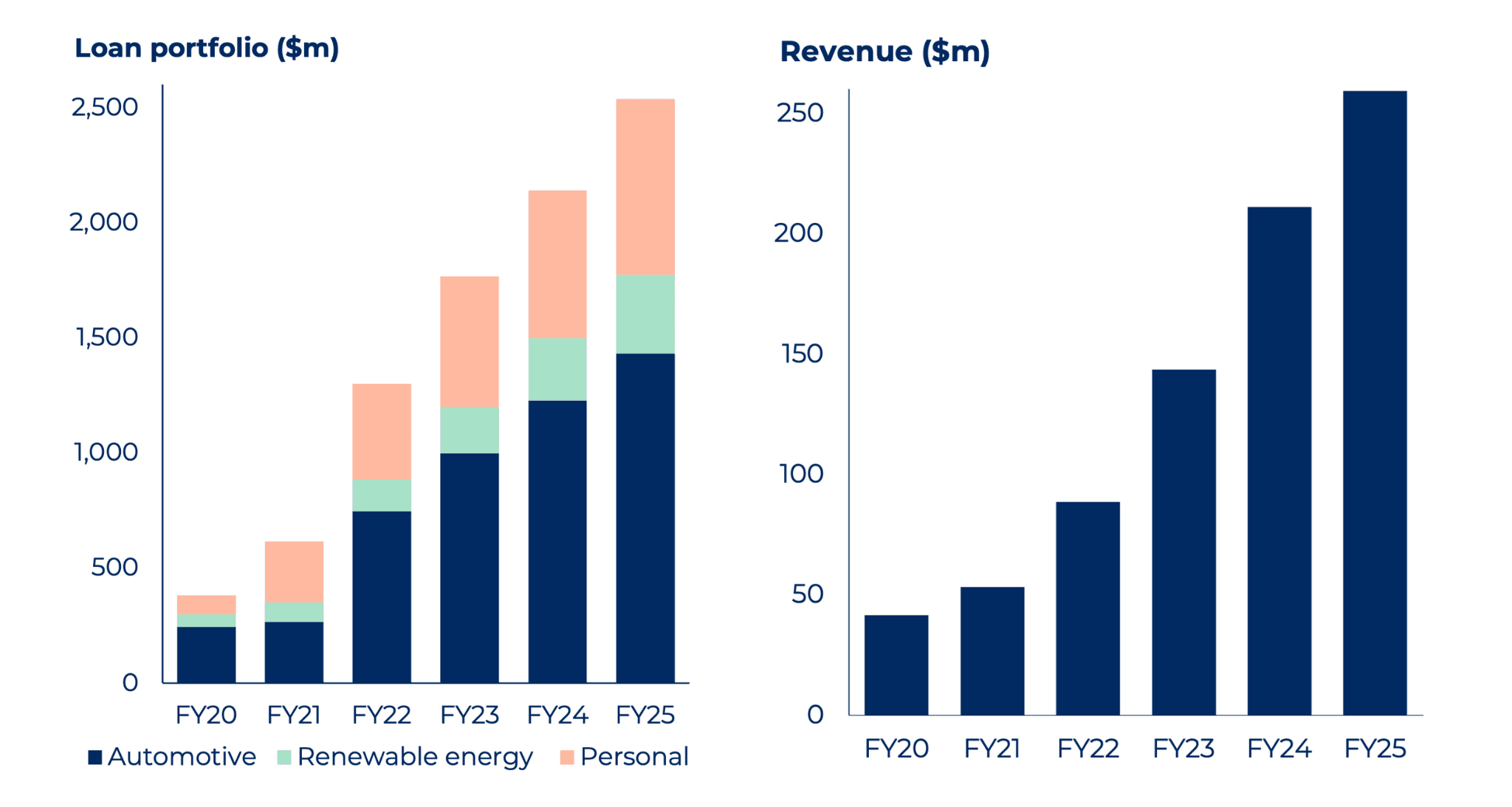

Loan portfolio and revenue growth

Plenti's diversified loan portfolio increased to $2.5 billion at 31 March 2025, up 19% from the prior comparable period (PCP).

The growth in Plenti's loan portfolio, combined with higher borrower interest rates, drove revenue to $259 million, up 23% on PCP.

Loan originations by lending vertical

Plenti's loan portfolio, which is a key driver of revenue and profitability, increased to $2.5 billion at 31 March, a 19% increase from 31 March 2024 and a 6% increase from 31 December 2024

Loan originations and margins

- Automotive loan originations were $709 million, up 14% on PCP, supported by the launch of a successful subvention program with Tesla

- Renewable energy loan originations were $189 million, up 18% on PCP, driven in part by the continued adoption of Plenti's GreenConnect platform, which is helping to accelerate uptake of household battery systems

- Personal loan originations were $519 million, up 24% on PCP, supported by further advancements in automated credit approvals as well as increased repeat and cross-sell origination volumes from existing borrowers

Technology enhancements

Plenti made regular enhancements to its technology platform during the year, including improvements to the customer experience, credit decisioning and pricing, partner integrations and operational process to increase efficiency. Pleasingly, these investments significantly improved our automated decisioning rates, with material loan application volumes now processed without human intervention. Plenti also continued to invest technology resources in the launch and roll out of the 'NAB powered by Plenti' car loan, facilitating increasingly meaningful volumes in 4Q25.

Consistent with prior years, all investment in product and technology – which amounted to $14.1 million in the year – was expensed through the profit and loss statement, rather than being capitalised on the balance sheet.

Credit performance

Plenti delivered another year of strong credit performance, reflecting our prime loan portfolio. The net credit loss rate for the full year was 1.10%, broadly consistent on PCP of 1.06%. This reflects Australian consumers having improved real income and low unemployment, as well as Plenti's continued focus on lending to borrowers with prime credit characteristics. Plenti completed its third sale of previously written-off loan receivables, which helped support loan recoveries in the period.

90+ day arrears were 0.43% at the end of the period, down from 0.58% at the end of the PCP, again reflecting the credit quality of Plenti's portfolio, ongoing refinement of credit rules and favourable macroeconomic conditions.

Lower-risk secured automotive loans and renewable energy loans together represented ~70% of the loan portfolio at the end of the period.

Margins, costs and profitability

Loan profitability and credit appetite continued to be a key focus during the year, given the sustained volatility in funding costs. Plenti's net interest margin for FY25 was 5.31%, up 14bps on PCP.

Plenti continued to benefit from the operational leverage inherent in its technology-led business model, materially reducing its cost-to-income ratio to 23.9% from 26.5% in the PCP.

The improvement in the cost-to-income ratio was supported by increased levels of automation across business activities such as credit approval which enhanced operational efficiency while providing faster, seamless service for partners and customers.

Cash NPAT for FY25 of $13.8 million represented an increase of 126% on PCP. The improvement in profitability was driven by 16% growth in the average loan portfolio and operating leverage (operating costs increased 11% on PCP), aided by slightly higher margins and stable credit losses.

Financial position and funding

Plenti completed three ABS transactions during the year for a total of $1.3 billion, making FY25 a record year for ABS issuance and taking issuance since program inception to over $3.4 billion. With supportive capital markets conditions and Plenti's growing track record as an issuer of high-quality debt securities, the business continued to expand and diversify its investor base with a record number of investors participating through the year.

Plenti funded its operations from business cashflows and recycling of existing capital during the period. The business generated underlying free operating cashflow of ~$12.5 million in FY25 which broadly offset the net $10.8m of capital invested into warehouse and ABS facilities ($44.5 million invested into warehouse facilities with $33.7 million released to Plenti).

Plenti extended the term of its corporate debt facility to support ongoing business growth. The facility limit is linked to the size of Plenti's securitised loan portfolio, providing an ability to access more capital with loan portfolio growth. A further $5.0 million was drawn under the facility during the year, although net debt remained stable at year end against March 2024.

Corporate cash at 31 March 2025 was $48.8 million or $26.5 million excluding customer collections account cash. This was up from $44.8 million ($20.8 million underlying) at 31 March 2024.

Strategic partnership with NAB

The 'NAB powered by Plenti' car loan, targeted to NAB's large personal banking customer base, was made available to NAB customers in late September 2024 with the expectation of contributing only moderate loan volumes in 2H25.

Important work was completed in 4Q25 to increase the visibility of the product to NAB customers, with the NPBP car loan made available via the NAB website, NAB banking app and internet banking portal. Volumes grew steadily across 4Q25, delivering a more meaningful contribution to loan book growth.

Volumes have accelerated further into 1Q26 with run-rate originations per business day in May month-to-date up 105% against average daily originations-rate in 4Q25.

Refreshed corporate strategy

Plenti refreshed its corporate strategy and commenced implementation during 4Q25.

Plenti currently operates as a relatively small player in large lending markets, providing significant growth opportunities. Plenti will pursue a 'breakout' growth strategy across three distinct horizons:

| Horizon 1 | Horizon 2 | Horizon 3 |

| Jan 2025 to March 2026 | April 2026 to March 2028 | April 2028 to March 2030 |

| GROW by doing what we do, but better | GROW by also doing new things | GROW by scaling boldly into new opportunities |

The three key elements of Plenti's corporate strategy which will be pursued across all three horizons are to:

- Strengthen relationships with our target customers and partners to ensure complementary and diverse distribution channels.

- Better use data and artificial intelligence to improve credit decisioning, reduce the cost of manufacture, optimise pricing, and substantially uplift new customer originations and cross-sell capabilities.

- Leverage our proprietary technology stack to provide customers and brokers with the fastest, easiest, simplest and most consistent journey available in market.

In Horizon 1, Plenti will focus on further uplifts to our experiences to offer faster, easier and simpler loan originations for customers and partners in our core lending verticals of Automotive, Renewables and Personal Lending, and to improve on all facets of our operations. Our objective in Horizon 1 is to achieve a loan book of $3 billion by March 2026, providing a strong foundation for the pursuit of a $ 5 billion loan book in the medium term.

FY26 objectives

Plenti's objectives for the year to 31 March 2026 are set out below:

| Priority | FY26 objective |

| Growth | - $3 billion loan book by March 2026 in Horizon 1 with acceleration of origination growth into Horizon 2 |

| Profitability | - Continue to drive meaningful Cash NPAT growth as we scale |

| Efficiency | - Deliver previously communicated $25 million of efficiency as loan portfolio scales towards $3 billion – ~$69 million operating cost base or less in FY26 |

Further information

This release was approved by the Plenti Board of Directors.